United States, New York, Nov. 28, 2024 (GLOBE NEWSWIRE) — Winds are stronger and more consistent further out to sea Close to 80% of the world’s offshore wind resource potential is in waters deeper than 60 meters. 2.4 billion people live within 100km of the shoreline – floating offshore wind can deliver major-scale power directly to global markets. Floating wind can potentially power 12 million homes in Europe by 2030.

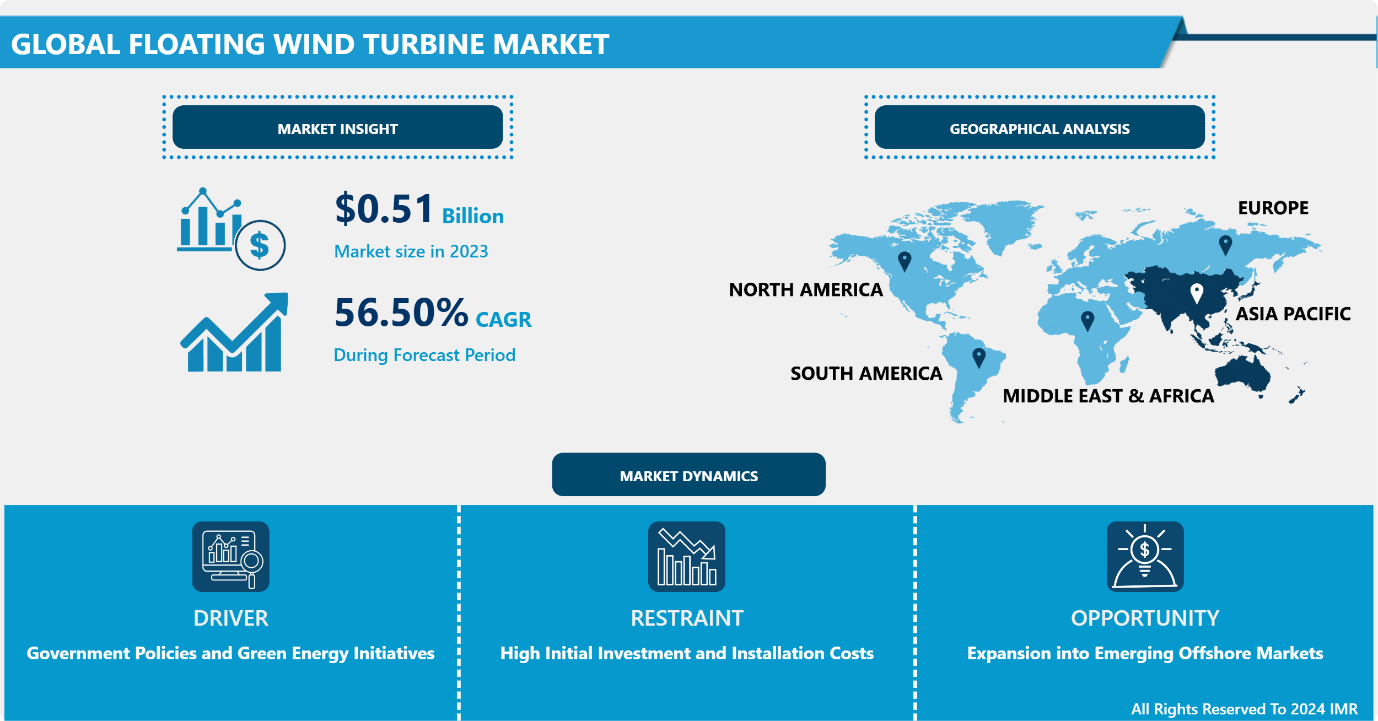

Introspective Market Research is excited to announce the launch of its latest publication, the “Floating Wind Turbine Market” report. This in-depth examination shows that the worldwide Floating Wind Turbine Market, valued at USD 0.51 Billion in 2023, is anticipated to increase substantially and reach USD 28.97 Billion by 2032. This strong growth translates to a solid compound annual growth rate (CAGR) of 56.50% from 2024 to 2032.

Offshore wind energy is a source of clean and renewable energy obtained by harnessing the power of the wind offshore, which reaches a higher and more constant speed due to the lack of barriers. Its high potential and strategic added value, both at a socioeconomic and environmental level, make it one of the renewable sources that will play a crucial role in the decarbonization process.

Floating offshore wind, based on floating structures rather than fixed structures, offers new opportunities and alternatives. Basically, it opens the door to sites further offshore by allowing the deployment of wind turbines in larger and deeper offshore areas with higher wind potential. It thus overcomes a stumbling block to providing clean, inexhaustible and non-polluting energy for a more sustainable planet.

Among the advantages of floating offshore wind are the potentially low environmental impact and the ease of manufacture and installation, as the floating turbines and platforms can be built and assembled on land and then towed to the offshore installation site. In addition, as noted above, they can take advantage of the strong winds blowing in the deeper areas, which improves energy efficiency.

Floating wind power is mounted on a floating structure in infeasible offshore locations where a fixed-foundation is difficult due to extreme water depths. Offshore wind power plays a significant role in achieving the renewable target in most countries worldwide. The floating wind power market is driven by increasing energy demand and adoption of renewables for energy production.

Download Sample 250 Pages Of Floating Wind Turbine Market Report@ https://introspectivemarketresearch.com/request/16940

Prominent Drivers of the Floating Wind Turbine Market

Abundance of Deepwater Wind Resources

The Floating Wind Turbine Market is driven by the ability to access deepwater wind resources, which are often characterized by stronger and more consistent wind speeds compared to onshore or shallow offshore sites. Traditional fixed-bottom wind turbines are limited to depths of approximately 50-60 meters, restricting them to nearshore installations. However, many regions around the world, including Japan, the west coast of the United States, and parts of Northern Europe, have significant wind resources located in deeper waters. Floating wind turbines are engineered to be anchored in water depths exceeding 60 meters, opening vast areas for energy generation.

These deepwater locations benefit from higher average wind speeds, which directly translate into greater energy output and higher capacity factors. Moreover, such locations typically face less interference from human activities and shipping routes, further enhancing efficiency and reducing conflicts. The ability to harness these resources is critical as global electricity demand continues to rise, especially with the shift towards clean energy sources. Floating wind turbines thus offer a scalable solution to expand renewable energy generation while addressing energy security concerns.

The opportunity to develop deepwater wind energy also aligns with the growing need for carbon-neutral energy sources. By utilizing floating turbines, countries can significantly increase their renewable energy portfolios, meeting ambitious climate goals and reducing greenhouse gas emissions. This capability makes floating wind turbines a cornerstone of future offshore wind energy strategies.

Technological Advancements in Floating Platforms

Technological innovation is a cornerstone of growth in the Floating Wind Turbine Market. Unlike fixed-bottom systems, floating wind turbines use specialized platforms such as spar-buoy, semi-submersible, and tension-leg designs, which are engineered to operate efficiently in deep and often turbulent waters. Each of these designs offers unique advantages. For instance, spar-buoy platforms are known for their stability, semi-submersibles for their adaptability to various seabed conditions, and tension-leg platforms for their ability to minimize motion even in harsh weather.

Advancements in materials and construction methods have reduced the costs of these platforms, making floating wind turbines more competitive with fixed-bottom systems and other renewable energy technologies. Moreover, improved mooring and anchoring systems ensure that turbines remain stable and can withstand challenging marine conditions. Dynamic cabling systems, which transmit generated power from the turbines to onshore grids, have also evolved to handle the movement of floating structures while maintaining efficiency.

These technological developments have not only lowered capital and operational costs but have also increased the reliability and lifespan of floating turbines. The ability to scale these platforms to accommodate larger turbines further enhances the market’s potential, as larger turbines can produce more energy, reducing the levelized cost of electricity (LCOE). This continuous innovation is critical to accelerating the adoption of floating wind turbines and making them a viable option for deepwater energy production.

“Research made simple and affordable – Trusted Research Tailored just for you – IMR Knowledge Cluster”

https://www.imrknowledgecluster.com/

Government Policies and Green Energy Initiatives

Supportive government policies and green energy initiatives are pivotal in driving the Floating Wind Turbine Market. Governments worldwide are increasingly recognizing the need to transition to renewable energy sources to combat climate change and achieve energy independence. Many nations have set ambitious targets for reducing greenhouse gas emissions, aligning with global frameworks such as the Paris Agreement. Floating wind turbines, with their ability to harness untapped deepwater wind resources, are an essential part of achieving these goals.

Financial incentives, including grants, subsidies, and tax benefits, have been introduced to encourage investment in floating wind technology. For example, the European Union’s Green Deal emphasizes offshore wind energy as a key component of achieving carbon neutrality by 2050. Similarly, the United States has launched initiatives under the Inflation Reduction Act to accelerate renewable energy development, including floating wind projects along its coasts.

In addition to financial support, governments are simplifying regulatory frameworks to streamline permitting and construction processes for offshore wind projects. Public-private partnerships are being promoted to foster innovation and reduce financial risks for developers. Moreover, national energy plans increasingly prioritize offshore wind energy, including floating turbines, to reduce dependency on fossil fuels and ensure long-term energy security.

These policies and initiatives not only incentivize market growth but also encourage the development of local supply chains, creating jobs and boosting economic growth. By addressing economic, environmental, and energy security goals, government support is a significant enabler for the widespread adoption of floating wind turbines.

How can the expansion into emerging offshore markets drive growth and innovation in the Floating Wind Turbine Market?

The Floating Wind Turbine Market presents a significant opportunity for expansion into emerging offshore wind energy markets, particularly in regions with deepwater coastlines. Countries such as Japan, South Korea, India, Brazil, and several African nations possess extensive deepwater areas where traditional fixed-bottom turbines are infeasible. These regions are witnessing growing electricity demand driven by industrialization, urbanization, and economic development. Floating wind turbines can play a critical role in meeting these energy needs sustainably.

Emerging markets often face energy challenges, such as reliance on imported fossil fuels or inadequate power infrastructure, making renewable energy solutions highly attractive. Floating turbines provide a scalable, renewable energy source that can be developed near population centers along coasts, reducing transmission losses and improving energy access. Furthermore, these projects align with global sustainability goals, making them eligible for international funding from climate-focused organizations and development banks.

Several governments in emerging markets are introducing policies and financial incentives to attract investment in offshore wind projects. For instance, Japan and South Korea have set ambitious offshore wind energy targets, creating a favorable environment for floating turbine adoption. Collaboration with international energy firms can accelerate technology transfer, local supply chain development, and workforce training.

High Initial Investment and Installation Costs

One of the significant challenges facing the Floating Wind Turbine Market is the high initial investment required for project development and installation. Unlike traditional fixed-bottom turbines, floating wind systems require specialized technology, such as advanced floating platforms, dynamic cabling, and robust mooring systems, to operate efficiently in deepwater conditions. These components, combined with the complexities of offshore installation, significantly increase upfront costs.

The cost of floating wind turbines is further compounded by the need for large-scale infrastructure, including purpose-built ports, specialized vessels for transportation and installation, and advanced grid connectivity solutions to transmit power from remote offshore locations to onshore networks. In regions where such infrastructure is underdeveloped, additional investments are required, creating financial barriers for new entrants and smaller companies.

Moreover, the floating wind industry is still in its nascent stages compared to fixed-bottom systems, leading to limited economies of scale. Many floating wind projects remain in the demonstration or pilot phases, and achieving commercial-scale deployments requires overcoming substantial financial and technological hurdles. Financing these projects often involves significant risks due to the uncertainties surrounding long-term performance and maintenance in harsh marine environments.

Key Manufacturers

Market key players and organizations within a specific industry or market that significantly influence its dynamics. Identifying these key players is essential for understanding competitive positioning, market trends, and strategic opportunities.

- General Electric

- Vestas

- Siemens

- Goldwind

- Shanghai Electric

- ABB

- Doosan Corporation

- Hitachi Ltd.

- Nordex SE

- EEW Group

- Nexans

- DEME

- Ming Yang Smart Energy Group Co

- Envision

- Rockwell Automation Inc.

- Hyundai Motor Company

- Schneider Electric

- Zhejiang Windey Co. Ltd.

- Taiyuan Heavy Industry Co.

- Sinovel Wind Group Co. Ltd., and Others Key Player

Do you need any industry insights on Floating Wind Turbine Market, Make an enquiry now >> https://introspectivemarketresearch.com/inquiry/16940

Recent Development

In January 2024, GE Vernova announced 1.4 GW of onshore wind projects with Squadron Energy in Australia. GE Vernova’s Onshore Wind business announced the signing of a strategic framework agreement with Squadron Energy for 1.4 gigawatts (GW) of onshore wind projects in New South Wales, Australia. Squadron Energy announced the agreement earlier this month, marking the commencement of construction of the Uungala Wind Farm.

In May 2023, GE announced that it would invest $50 million in its Schenectady, NY, facility and hire about 200 additional full-time employees, including skilled union operators, manufacturing engineers, and front-line leadership, to develop a new manufacturing assembly line for its onshore wind business. The facility will assemble three essential components for GE Vernova’s 6.1 MW turbine.

Key Segments of Market Report

By Capacity:

Turbines with capacities above 5 MW are emerging as the dominant segment, capturing a significant market share during the forecast period. This dominance stems from a strategic emphasis on meeting the rising demand for enhanced energy production efficiency in offshore wind farms. With the global push towards renewable energy intensifying, maximizing energy output per turbine has become a critical objective to harness the vast wind resources available offshore effectively.

To achieve this, developers and participants are increasingly adopting high-capacity turbines equipped with larger blades, enabling greater power generation. These turbines enhance the energy density per unit, boosting the overall competitiveness and longevity of offshore wind projects. The adoption of higher-capacity turbines reflects a broader industry shift towards optimizing energy yield and ensuring the sustainability of offshore wind farms.

Technological advancements further fuel the rise of the 5 MW+ segment. Manufacturers are pioneering next-generation turbines incorporating innovations such as larger rotor diameters, reinforced drivetrain systems, and aerodynamic enhancements. These improvements not only enhance energy capture but also reduce the Levelized Cost of Energy (LCOE) for offshore wind infrastructure, making floating turbines more economically viable.

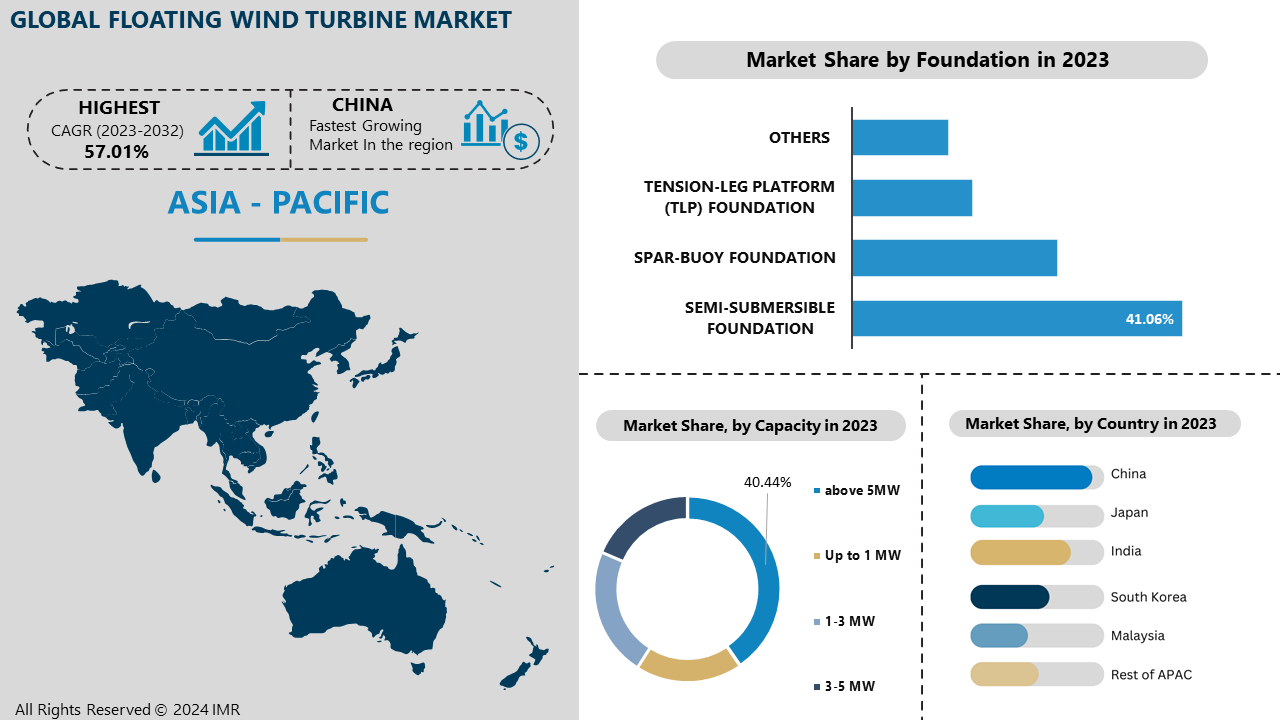

By Foundation:

The semi-submersible foundation sub-segment dominates the floating wind turbine market due to its unique combination of versatility, cost-effectiveness, and scalability. Designed to float and remain buoyant in deep waters, semi-submersible platforms are highly adaptable to varying water depths and seabed conditions, making them suitable for deployment in a wide range of offshore locations. This adaptability gives them a significant edge over other foundation types like spar-buoys or tension-leg platforms, which may have stricter site requirements.

Semi-submersible platforms are often pre-assembled at ports before being towed to installation sites, reducing the complexity and cost of offshore construction. This feature simplifies logistics and shortens project timelines, a critical advantage in scaling up offshore wind projects. The ability to use common installation vessels and equipment further minimizes costs compared to other floating foundation types.

Semi-submersible foundations offer a stable platform even in challenging marine environments with high waves and strong winds. Their design distributes weight evenly, ensuring that turbines remain operational under dynamic conditions. This stability is essential for maximizing energy production and minimizing downtime.

By Region

The Asia-Pacific (APAC) region dominates the floating wind turbine market due to its combination of abundant offshore wind resources, supportive government policies, and a growing focus on renewable energy development. These factors position APAC as a leader in the adoption and deployment of floating wind technology.

APAC boasts extensive coastlines with significant deepwater areas, particularly in countries like Japan, South Korea, China, and Taiwan. These regions have strong and consistent wind speeds, ideal for floating wind turbines that can be deployed in water depths exceeding the limitations of traditional fixed-bottom systems. For instance, Japan’s mountainous seabed restricts fixed-bottom turbines, making floating solutions essential for harnessing its vast offshore wind potential.

Governments in APAC are actively promoting offshore wind energy to meet ambitious renewable energy targets and reduce dependency on fossil fuels. For example, Japan and South Korea have set substantial offshore wind capacity goals, and China is rapidly expanding its offshore wind infrastructure. These countries provide financial incentives, subsidies, and streamlined permitting processes to attract investment in floating wind projects.

The region’s growing population and industrialization drive an increasing demand for clean energy solutions. Floating wind turbines provide a scalable and sustainable option to meet this demand, particularly in countries with limited land availability for onshore renewable projects.

If you require any specific information that is not covered currently, we will provide the same as a part of the customization >> https://introspectivemarketresearch.com/custom-research/16940

Comprehensive Offerings:

- Historical Market Size and Competitive Analysis (2017–2023): Detailed assessment of market size and competitive landscape over the past years.

- Historical Pricing Trends and Regional Price Curve (2017–2023): Analysis of historical pricing data and price trends across different regions.

- Market Size, Share, and Forecast by Segment (2024–2032): Projections and detailed insights into market size, share, and future growth by segment.

- Market Dynamics: In-depth analysis of growth drivers, restraints, opportunities, and key trends, with a focus on regional variations.

- Market Trend Analysis: Evaluation of emerging trends that are shaping the market landscape.

- Import and Export Analysis: Examination of trade patterns and their impact on market dynamics.

- Market Segmentation: Comprehensive analysis of market segments and sub-segments, with a regional breakdown.

- Competitive Landscape: Strategic profiles of key players across regions, including competitive benchmarking.

- PESTLE Analysis: Evaluation of the market through Political, Economic, Social, Technological, Legal, and Environmental factors.

- PORTER’s Five Forces Analysis: Assessment of competitive forces influencing the market.

- Industry Value Chain Analysis: Examination of the value chain to identify key stages and contributors.

- Legal and Regulatory Environment by Region: Analysis of the legal landscape and its implications for business operations.

- Strategic Opportunities and SWOT Analysis: Identification of lucrative business opportunities, coupled with a SWOT analysis.

- Conclusion and Strategic Recommendations: Final insights and actionable recommendations for stakeholders.

Related Report Links:

Circular Economy Market: Circular Economy Market Size Was Valued at USD 3.1 Trillion in 2023 and is Projected to Reach USD 6.3 Trillion by 2032, Growing at a CAGR of 8.20 % From 2024-2032.

Turbines Market: Turbines Market Size is Valued at USD 238.0 Billion in 2024, and is Projected to Reach USD 370.95 Billion by 2032, Growing at a CAGR of 5.70% From 2024-2032.

Synchronous Wind Turbine Tower Market: Global Synchronous Wind Turbine Tower Market Size Was Valued at USD 8.91 Billion in 2022 and is Projected to Reach USD 16.43 Billion by 2030, Growing at a CAGR of 8.01% From 2023-2030

Smart Waste Market: Smart Waste Market Size Was Valued at USD 2.66 Billion in 2023, and is Projected to Reach USD 10.27 Billion by 2032, Growing at a CAGR of 16.20 % From 2024-2032.

Hydropower Generation Market: Hydropower Generation Market Size Was Valued at USD 251.75 Billion in 2023 and is Projected to Reach USD 424.24 Billion by 2032, Growing at a CAGR of 5.97% From 2024-2032.

Renewable Energy Market: Renewable Energy Market Size Was Valued at USD 1.39 Billion in 2023 and is Projected to Reach USD 2.77 Billion by 2032, Growing at a CAGR of 7.95% From 2024-2032.

Hydrogen Generation Market: Hydrogen Generation Market Size Was Valued at USD 152.87 Billion in 2023, and is Projected to Reach USD 326.03 Billion by 2032, Growing at a CAGR of 8.78% From 2024-2032.

Concentrated Solar Power Market: Global Concentrated Solar Power Market was valued at USD 7.60 billion in 2023 and is expected to reach USD 14.83 billion by the year 2032, at a CAGR of 7.71%

Bio LPG Market: Bio LPG Market Size Was Valued at USD 434.93 Million in 2023, and is Projected to Reach USD 7341.16 Million by 2032, Growing at a CAGR of 36.89% From 2024-2032.

Bio Coal Market: Bio Coal Market Size Was Valued at USD 159.05 Billion in 2023, and is Projected to Reach USD 271.46 Billion by 2030, Growing at a CAGR of 6.12 % From 2024-2032.

About Us:

Introspective Market Research is a premier global market research firm, leveraging big data and advanced analytics to provide strategic insights and consulting solutions that empower clients to anticipate future market dynamics. Our team of experts at IMR enables businesses to gain a comprehensive understanding of historical and current market trends, offering a clear vision for future developments.

Our strong professional network with industry-leading companies grants us access to critical market data, ensuring the generation of precise research data tables and the highest level of accuracy in market forecasting. Under the leadership of CEO Mrs. Swati Kalagate, who fosters a culture of excellence, we are committed to delivering high-quality data and supporting our clients in achieving their business goals.

The insights in our reports are derived from primary interviews with key executives of top companies in the relevant sectors. Our robust secondary data collection process includes extensive online and offline research, coupled with in-depth discussions with knowledgeable industry professionals and analysts.

Contact Us:

Canada Office

Introspective Market Research Private Limited, 138 Downes Street Unit 6203- M5E 0E4, Toronto, Canada.

APAC Office

Introspective Market Research Private Limited, Office No. 401, Saudamini Commercial Complex, Kothrud, Pune, India 411038

Ph no: +91-81800-96367 / +91-7410103736

Email: sales@introspectivemarketresearch.com

LinkedIn| Twitter| Facebook | Instagram

Ours Websites : https://introspectivemarketresearch.com | https://imrknowledgecluster.com/knowledge-cluster | https://imrtechsolutions.com | https://imrnewswire.com/ | https://marketnresearch.de |