One sector that has managed to thrive in every global climate is the automotive industry.

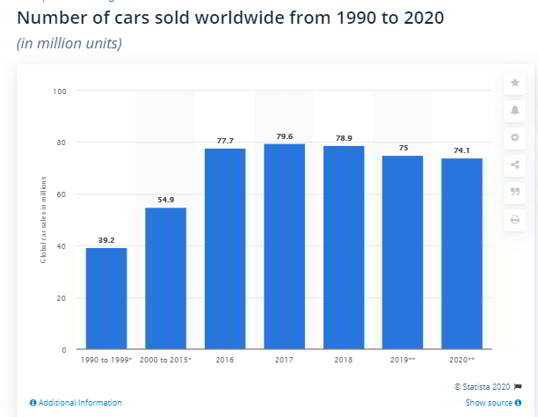

According to Statista, 74.1 million new cars will be sold around the world in 2020. While global car sales keep increasing, what is changing is how consumers purchase cars.

Yes, buying a car continues to be an exhilarating experience. It feels empowering. After all, being a car owner is much more than merely providing yourself with a mode of transport. It illustrates your independence and establishes your status.

But, now, people are more inclined to purchase used vehicles than new ones. As per a survey conducted by Cox, over 64 percent of respondents prefer buying used cars compared to 35 percent of people who wish to purchase new ones.

One of the biggest reasons for this trend is the considerably high price of most new cars. If you wish to purchase a new car, you might find yourself short of funds. However, what a lot of people don’t know is that there are various car financing options you can explore before settling for a used vehicle.

Here is a quick guide that can help you in deciding on a car finance option!

1. Dealer Financing

When you visit a dealership to purchase a car, they will provide you with different dealer financing options. This includes Personal Contract Purchases, Hire Purchases, and Personal Leasing. Almost every car dealer offers these solutions.

It is imperative that you know what each of these financing options entails before you pick one.

In Personal Contract Purchases, dealers will ask you for a lump sum upfront deposit, which can be viewed as a down payment. Another lump sum will be charged to close the purchase. The remaining amount is then distributed evenly across a given number of months.

After you have paid the installments, you can either return the vehicle to the dealer or sell it to pay the closing lump sum amount. In this financing option, the dealer charges the minimum future value rather than the sticker price.

In Personal leasing, again, you have to make an upfront payment and pay the remainder in installments. It also puts limitations on car mileage. But, while at the end of a Personal Contract, you end up owning the car, this is not the case with leasing. Here, you are given the option to switch to another vehicle.

Depending on the dealership, you might be offered service benefits to help you in taking care of the car. All of it comes at the cost of a fixed annual percentage rate levied on your payments.

In Hire purchases, you are required to pay monthly payments and an interest rate as well. Just like the other two options, here too you own the car once you have paid its full sticker price. Because of the interest charge involved, this financing option is significantly pricier than the other two options.

Be careful!

You must be cautious when opting for dealer financing. This is because, in an effort to boost their revenue, dealers will try to persuade you to opt for additional options and services on top of your plan. Each benefit comes with an additional cost.

So, make sure you are certain that you need a given service or not. For instance, are they offering auto insurance at rates you don’t need? Refuse if so.

2. Credit Cards

Apart from car financing plans offered by dealerships, there are various independent financing options you can explore.

For starters, you can make use of credit cards. Let’s say you see Tom Hartley cars for sale in a dealership but don’t like the financing options they give you. This is because you want quick ownership of the vehicle.

In such a case, credit cards will come in handy. A credit card will allow you to purchase the car upfront. You will then have to pay back the loan to the credit card provider on top of an interest rate charged.

Generally, this financing method is cheaper than dealership financing since the interest rates offered by credit cards are lower.

However, this may or may not be the case for you since interest rates charged on credit cards increase if your credit score deteriorates. It all depends on your credit history. Compare the cost of buying the vehicle via a credit card versus through leasing.

3. Personal Loans

Just like credit cards, seeking a personal loan helps you in sealing the transaction upfront. You can gain ownership of your car and then pay back to the bank or your lender at a predetermined interest rate and time period.

Personal loans are an excellent financing option since they don’t require a lump sum payment at the beginning of the plan. But, the downside is that the interest rate charged will be significantly higher in personal loans compared to dealerships.

Also, whether or not you get the loan will depend on your credit score. And the process will take time.

Which is the best?

Each car financing option has its pros and cons. Also, each solution is tailored for a given type of consumer.

For instance, Personal Contract Purchases are best suited for those individuals that like changing their vehicles every few years. A credit card is a suitable option for those who have an excellent credit rating. Personal loans will work for those who require immediate ownership of their vehicle and do not mind considerably time-consuming processing of the loan.

So, no one option is superior to the others. To make sure you select the right ones, compare the cost attached to each of the plans.

Try to negotiate the best deal for yourself. Remember, there is always room for such negotiations with dealers since they quote a price and plan with a significant profit margin for themselves.

So, do your research and understand where you stand in terms of your credit rating. This will allow you to make an informed decision.

With the different financing options now in front of you, you can now get yourself the car of your dreams.

Author Bio:

Evie harrison is a blogger by choice. She loves to discover the world around her. She likes to share her discoveries, experiences and express herself through her blogs. Find her on Twitter:@iamevieharrison

Super website good to read about the car Finance option